When you start fundraising, the universe is a big blob of potential investors.

A lead investor typically anchors the round and helps set terms that other investors follow.[1][2]

So you take meetings.

If it's your first rodeo, you'll get a lot of "no" because:

- Wrong type of company for the fund

- Wrong stage ("you're a bit early for us")

- Portfolio conflict

- They just don't know your space

- They do know your space and think you're meh (this is the most common reason, hate to break it to you)

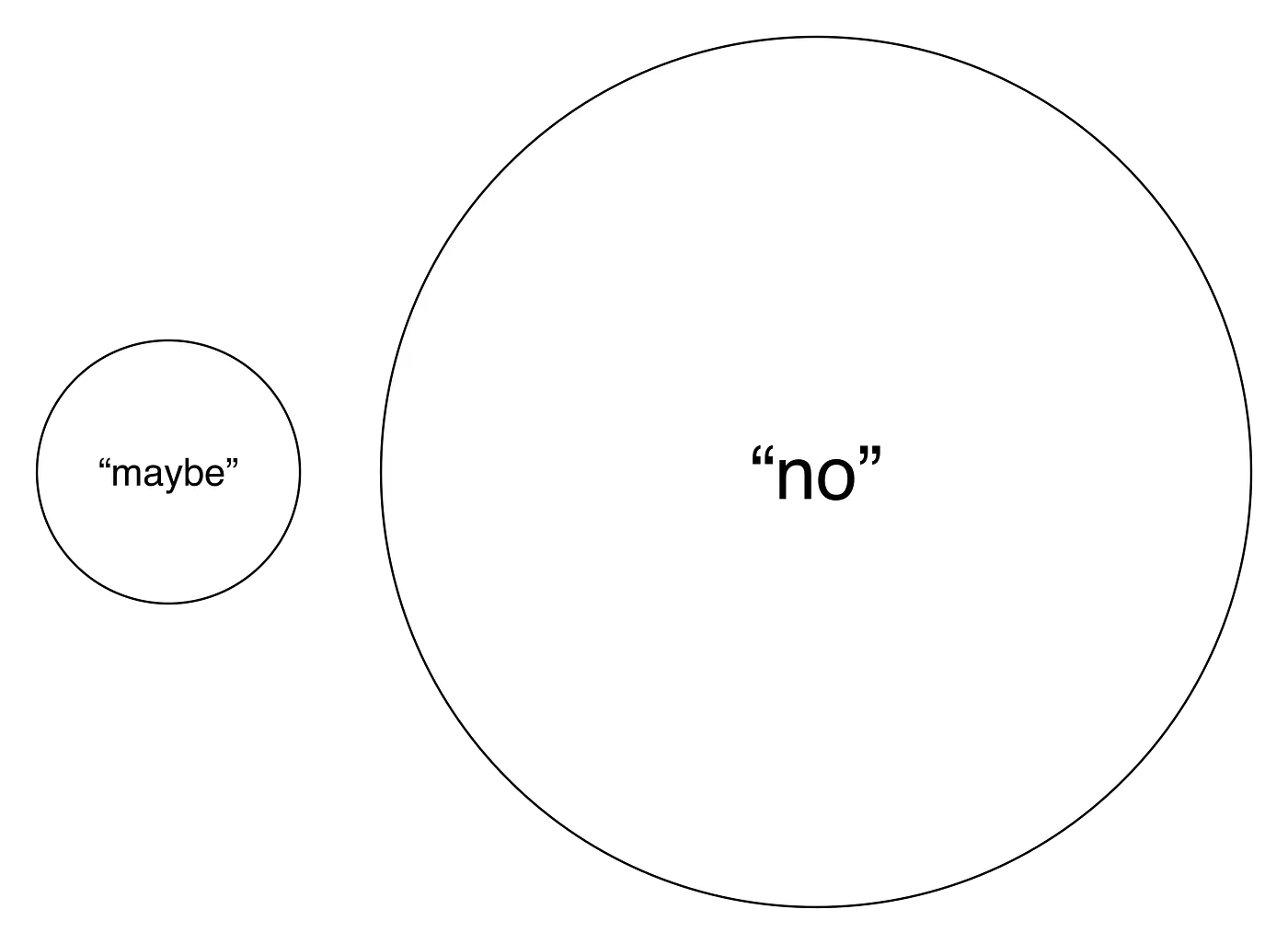

So you end up with a pile of "no" and a smaller pile of "maybe."

The quality of your investment opportunity—team, product, market, traction, pitch—determines these ratios.

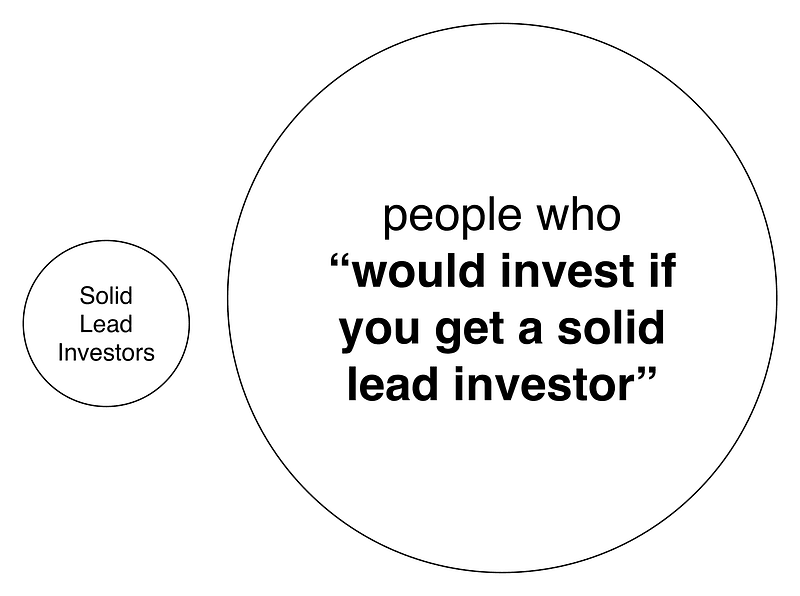

Digging into your pile of "maybe," you discover that only a few are potential lead investors. The rest tell you they'd invest "if you find a solid lead."

And you'll discover that most of the strong investors (who are likely to lead) are already in your "no" pile. Because they're rockstars. They're pickier.

At this point, if you have too few potential leads, it's hard to create FOMO—and therefore hard to get term sheets. You're sorta screwed.

If you sort through your "maybe" pile and there's no potential solid lead, it's settled: you're not ready for an institutional round. Go back to the best investors you spoke to, find out why they said no, and get back to work — usually that means tightening up the four pillars of a seed-stage pitch.

Repeat this process until you find a lead investor.

Simple, eh? 😀

— Ry

Related Essays

Our Review of AngelPad: "Game Changing"

Our journey through AngelPad as the first Midwest team ever accepted. From application to Demo Day, here's what the top-ranked accelerator is really like.

The Four Pillars of a Seed-Stage Pitch

Every funded seed pitch crystallizes around four elements — product, team, traction, market. Miss any of them and the rest of the deck cannot rescue you.

The Fatal Pitch Mistakes (and What Actually Lands)

The three mistakes that sink fundable companies — setup-slide death, sanitized corporate-speak, and slide dependency. Plus what actually intrigues investors.

Key takeaways

- Fundraising is a funnel of no's and maybes.

- Without a potential lead, a round stalls.

- Use feedback to improve before re-raising.

FAQ

What is a lead investor?

The investor who anchors the round and sets terms. Others follow their lead.

What if I have no leads?

Pause, improve the company, and try again. Build enough momentum to create a real lead.